A review of Housing policy in Australia: a case for system reform by Hal Pawson, Vivienne Milligan and Judith Yates (Palgrave Macmillan 2020)

Last updated 15 July 2023

An indispensable starting point for any discussion of housing policy in Australia is Housing policy in Australia: a case for system reform by Hal Pawson, Vivienne Milligan and Judith Yates (Palgrave Macmillan 2020). This book by three of Australia’s leading housing analysts is the first comprehensive overview of housing policy in Australia in 25 years. It deserves to be read in full. Here nonetheless are the most important takeaways for me:

- Between 1945 and 1975, ‘Housing became a prominent component of the now long-lost contract between what used to be called ‘capital’ and ‘labour’ with overt government support for housing being a ‘fourth pillar’ of the post-war political settlement, alongside wages growth, social security and trade protection’ (Foreword by Bill Randolph, p. v). This reflected a bipartisan post-war commitment to secure and affordable housing as a fundamental platform for social and economic participation. Rent control and controls on bank lending were part of the deal.

- The neo-liberal ‘turn’ in policymaking that gained ascendancy from the late 1970s abandoned this commitment in favour of an overriding belief in the ‘efficiency’ of the ‘free market’ as opposed to the supposed inefficiency and undesirability of government intervention. The state out, the market in; this is still the dominant policy paradigm today, over 40 years later.

- The results? Yes, they are in: ‘housing has been turned into a financialised and debt-fuelled speculative asset class in which prices have decoupled from household incomes’; ‘housing debt and housing unaffordability at unheralded and unsustainable levels’; ‘rising homelessness and levels of housing stress’; ‘a residualised and degraded public housing sector’; ‘a failing home ownership market’; ‘growing reliance of the younger generation on insecure private renting’; ‘a crisis of confidence in the quality of high-rise multi-unit housing’; failure to recognise the ‘need to somehow retool our housing stock to deal with the challenge of climate change’; policy debate ‘increasingly driven by vested interest groups outside government, in particular a highly organised, resourced and vocal property lobby which never wastes an opportunity to press for less regulation, less oversight and greater tax breaks for private sector interests’ (Foreword, p. vi).

- ‘Necessary actions … extend well beyond the restricted market-enabling remit that generally determines policy legitimacy under the neo-liberal governance paradigm … any serious effort to confront housing unaffordability demands a more pro-active and socially responsible state that promotes a fairer housing tax and policy regime’ (p. 341).

- The authors define housing policy as ‘government actions or policy settings that influence (a) the supply of dwellings and its spatial distribution, (b) the characteristics and management of housing stock, and (c) who gets access to housing and on what terms’ (p. 9).

The authors summarise their case for urgent action on pp. 339-341:

continued on p. 341: ‘are unaffordable (Section 3.3.3). Augmenting the population cohort in after-housing poverty, people counted as homeless increased by 30% to 116,000 in the fifteen years to 2016 (ABS 2018).’

Given that ‘affordable housing is increasingly recognised as a key infrastructure requirement for the productivity of cities and regions, as well as being crucial to enhancing social cohesion, health and well-being’ (p. 292), this is a dire situation.

The authors posit a ‘housing system’ in reciprocal interaction with ‘a broader societal system’ (p. 6). Does the book adequately describe these systems and their interactions? For me, no, not quite. A number of questions are not tackled in the book. They need to be because for me they go to the heart of ‘the system’. Let’s work through the missing questions.

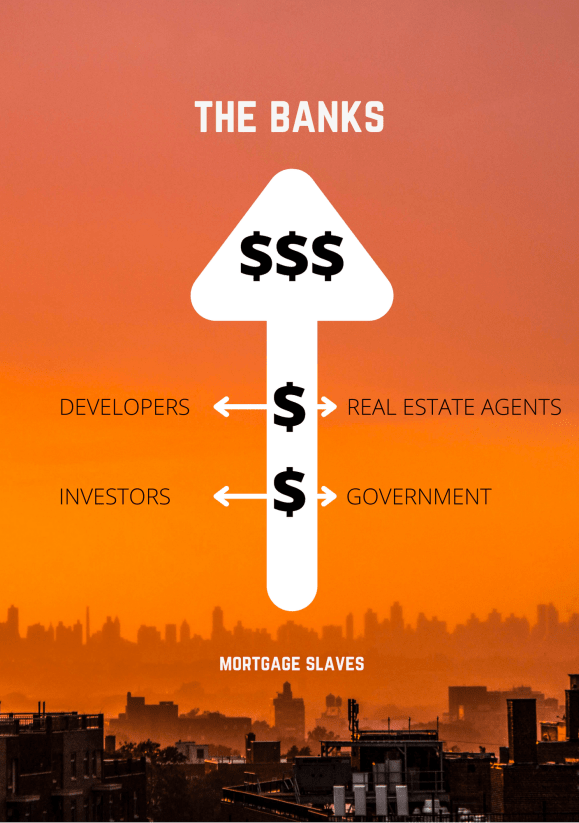

Who is making the most money out of the housing market in Australia?

Housing has been financialised so let’s follow the money. What are the $$ flows? We know the players: governments, banks and other financial institutions, developers, builders, real estate agents, valuers, lawyers, landlords, households, landowners –– some individuals and entities are more than one type of player. Who are the winners, who are the losers in $$ terms?

Private renters to landlords

Chris Martin in The Conversation, 8 April 2020, provided a figure for $$ flowing from private renters to their landlords:

‘Private renters [about 2.5 million Australian households] pay about A$43 billion a year in rent to another, smaller group of households: Australia’s 1.3 million landlord households. A little more than half of that rental income, A$22 billion, flows right out again to banks, as interest payments on investment loans. For 60% of landlords the interest outflow, plus other property-related expenses, is greater than their rental income: they are negatively geared. For them, rental income is not about putting food on the table; it is part-funding their investment or speculation in property.’

This flow of $ from private renters to landlords keeps increasing year by year as ‘Australia has seen a gradual decline in owner-occupation and in public housing over the past two decades, while the rate of private rental has significantly increased’ (Pawson et al, p. 12). And ‘In present day Australia private landlords are largely free to set rents at the level the market will bear’ (Pawson et al, p. 200). [‘Pawson et al’ is used hereafter to refer to Housing policy in Australia 2020.]

Government to landlords

Federal income tax settings over the past 20 years, in particular the negative gearing and Capital Gains Tax discount provisions, incur an annual cost to the public purse estimated to be $7.7 billion (Australia Institute) or $11.7 billion (Grattan Institute) –– (Pawson et al, p. 191). These tax concessions for landlords mainly benefit the already wealthy (Pawson et al, p. 196).

Home owner-purchasers to banks

‘In Australia, as in many other countries, the past 20 years have seen substantial real increases in residential property prices that, supported by an increased flow of mortgage lending after financial deregulation [which began in Australia in the 1970s and accelerated in the 1980s], have led to a marked rise in household indebtedness’ (Pawson et al, p. 38). ‘… Australian banks’ exposure to residential property is the highest in the developed world’ (Pawson et al, p. 39). What then have been the $$ flows to banks from home owner-purchasers over the last 20 years? This will be the biggest $$ flow of all I suspect, many billions if not trillions.

Where the $$ go:

just guessing

Home owner-purchasers to government

State governments collect stamp duty from home owner-purchasers. What have the $$ amounts been over the last 20 years? What are all the other $$ flows to government under current housing market arrangements, across all housing tenures?

$$ flows to real estate agents

What have these been over the last 20 years?

$$ flows to developers and builders

What have these been over the last 20 years?

Aged care residents to owners of aged care facilities

Gabrielle Meagher, in ‘A Genealogy of Aged Care in Australia’, Arena, No. 6, Winter 2021, p. 50, reported that in 2018-19 there was a ‘… $30 billion pool of ‘refundable accommodation deposits’ (commonly called ‘accommodation bonds’) that 95,000 [aged care] residents had contributed as interest-free loans to the owners of the facilities they live in, in lieu of paying a daily rate for their accommodation.’ Similar interest-free loans are provided to the owners of retirement villages by residents of these villages –– does anyone know the amount of these loans for Australia as a whole?

In a housing system that is all about the $$, we can’t fully understand ‘the system’ until all the $$ flows are quantified, and the flows need to be documented in more detail than the rough sketch I have suggested here. What is clear is that at every stage of our lives, from leaving our parents and renting a place somewhere, to buying our first home, to moving into a retirement village or aged care home, predators and parasites are lined up waiting for us, all wanting their cut, their share of the loot.

The elephant in the room

Pawson et al fail to mention that a key lever available to the Federal Government is the Council of Financial Regulators. (Table 1.3, p.22, makes no mention of it. Similar tables provided elsewhere by AHURI also omit this Council.) This is a serious omission. Financial regulation, of bank lending in particular, is a key determinant of house prices. I elaborate on this in my draft Green Paper below. The work of Adair Turner is instructive on this issue and I attach below some quotes from his book Between debt and the devil:

What is the quality of Australian housing?

There are objective criteria for the measurement of housing quality: structural integrity, life expectancy, energy efficiency, water efficiency, resource use sustainability, toxicity (asbestos, lead, VOCs), resistance to termites, resistance to mould and rising damp, insulation from road and air traffic noise and pollution, suitability for young and old, and for the disabled, natural light and ventilation, design with both privacy and opportunities for social interaction with neighbours in mind, access to community gardens, parks and sports fields, resistance to extreme weather and climate risks such as bushfires, flooding, hailstorms, coastal inundation, cyclones and subsidence … Other criteria could be added, some more difficult to measure: Are residents of the house forced to own a car to get to work, school, shops, sports facilities and other recreational venues? Are walking and cycling attractive options? Is safe, convenient, affordable public transport an option?

The fact is no level of government in Australia (local, state or federal) maintains a database of housing quality. The Shergold – Weir report (2018) on the building industry in Australia made some damning observations based on survey results. Geoff Hanmer from UNSW has written extensively on building quality in The Conversation <theconversation.com/au> and he too finds little to encourage confidence. Politicians nonetheless continue to parrot the view that there are ‘a few bad apples in the box’ but otherwise all is well –– a view not based on any reliable data.

Housing quality is an integral part of the housing system. Without a comprehensive national database of housing quality in Australia, this important aspect of the system remains in the shadows. Deregulation of the housing construction industry appears to have resulted in declining standards of building construction. Hypothesis: Malpractice in the building industry has resulted in quick profits for the industry and left communities and governments with defect remediation costs they will have to bear for decades to come.

Housing is now a very expensive commodity. What protects consumers?

The short answer is very little. House prices and rents bear no relation to the quality of houses for sale or rent. Prices have gone sky high; construction quality is heading towards rock bottom and the quality of existing housing stock is highly questionable. There is no independent statutory authority that does due diligence on properties for sale and provides the results to prospective buyers: pest and building inspections, inspections of title records, body corporate records and so on. Nor is anything provided either on the life expectancy of a dwelling or on many of the other criteria of housing quality listed above. Such an authority could simultaneously develop and maintain a national database of housing quality in Australia. Buyers have to do, in a very short timeframe usually, the due diligence themselves and pay for it even though, in a competitive bidding process, there is no guarantee they will be the successful bidder. Gazumping is common and, as I write this in mid-2021, buyers who can’t be bothered doing any due diligence are the kind of bidders preferred by sellers and real estate agents. The competitive bidding process, with auctions an increasingly common form of this, also contributes to upward pressure on prices. With no regulation of house prices or rents, the market rules; buyer protections are considered unnecessary ‘red tape’.

So how does ‘the system’ appear when we have answered these questions?

The perfect crime is one that no one recognises as a crime. The housing market is a lucrative trade in defective goods but I have never seen it described like that. What we have is daylight robbery, a housing heist, with key players such as banks, landlords, developers and others able to extract extraordinary wealth from a hapless population. We have a grotesque scam that is orchestrated primarily by the banks, aided and abetted by government, and cheered on by the shamans in suits, the economists, who tell us what we have is ‘jobs, investment, growth’. Is this the ‘animal spirits’ of capitalism let loose in the housing market? It seems more like a feudal arrangement, with privileged groups able to extract wealth from a captive population as they please, unfettered by any superordinate state controls. This is ‘the system’, all the more powerful because it is not recognised for what it is, a heist. It is a system of exploitation of the many by the few, a giant suction pump moving $$ to the wealthy few. In the jargon of economics, these people are making money without really adding value; they are in other words extracting economic ‘rent’. How and why such a system obtained a social licence and came to pass as ‘normal’ is for the sociologists and historians to work out. How such a state of affairs will affect the ‘resilience’ of our cities as they are smashed by climate change is for all of us to ponder. But no one is going to take my views seriously. Gary who? What we need is some kind of public interest lobby group, and that’s the next question.

A national housing advisory panel: what should it look like?

Government entities ‘will need to be supported by advisory bodies that enable wider stakeholder participation in policymaking and can offer specialist advice in priority areas such as affordable housing, homelessness, Indigenous housing and tax reform’ (Pawson et al, p. 352-3). A National Affordable Housing Alliance formed in 2020 appears at first glance to fit the bill. The core members of the Alliance are: Housing Industry Association, National Shelter, Property Council of Australia, Community Housing Industry Association, Australian Council of Trade Unions, Australian Council of Social Services, Master Builders Australia, Industry SuperAustralia, and Homelessness Australia. Yet can a body like this be trusted to represent the public interest rather than sectoral interests? Note also that The Australian Housing and Urban Research Institute (AHURI) and representatives from its national network of university research partners are absent.

A body with the public interest at heart and a solid research base would comprise instead: National Shelter, Community Housing Industry Association, Australian Council of Social Services, Industry SuperAustralia, Homelessness Australia, the Australia Institute, the Grattan Institute, AHURI and its research partners. Its first task would be to produce a Green Paper, the traditional prelude to a White Paper. Both of these tasks are usually the preserve of government. With government having absconded from the stage, however, the task of a Green Paper falls to civil society.

What does a Green Paper look like?

It’s not an academic paper. It’s compact, no more than 50 pages, preferably less, written in bureaucratese (lots of dot points) and structured in such a way that it can eventually form the basis of a White Paper, an official government policy document. Green Papers nowadays tend to be like public relations documents but in essence they need to address a number of key questions as follows:

- What are the problems? Who says so? What will happen if nothing is done?

- Objectives. What do we want the situation to be in the future? How will we know when our objectives have been achieved?

- Alternative strategies. What are all the possible ways to solve the problems, without prejudging their feasibility?

- Decisions. Cost – benefit analyses. Feasibility assessments. Who needs to be involved in deciding which strategies are best?

- Implementation. What arrangements need to be made with relevant state and non-state actors to implement the decisions? How will the needed resources be found? What timeframes will be adopted?

- Evaluation. Measuring progress and adjusting strategies in response.

A good example of how to proceed with “citizen-led” public policy is the lead-up to the National Anti-Corruption Commission:

- A model of best practice was developed by several key non-government bodies: Transparency International, Australia Institute, Centre for Public Integrity, The Greens …

- A campaign was conducted by these bodies over several years to publicise and argue for the model.

- A search was conducted for Federal MPs who would champion the model. Helen Haines, Zali Steggall, Larissa Waters and others were found.

- The MPs then drafted legislation that would best give effect to the model and tried continuously to get it through the Parliament.

- Labor finally felt compelled to do something …

- Because a model of best practice existed, Labor’s version could be evaluated in terms of that best practice model.

Housing policy is more complex but a similar approach needs to be adopted. Until we have a version of housing policy that key bodies (not the ones making money out of the housing market) accept as the best way to go, we are really just treading water.

I’ve had a go at a housing Green Paper and you can download it below. I’ll keep updating it; latest update 15 July 2023.